- November 15, 2022

- Posted by: CoachShane

- Category: Trading Article

If you’re new to options trading, you may have come across the term “implied volatility” and wondered what it means. In this blog post, we’ll give you a brief overview of implied volatility and how it’s used by options traders.

Key Points

Using implied volatility can help you determine whether an options contract is overpriced or underpriced.

It can also help you predict how volatile the underlying security will be in the future.

Implied volatility can help you decide when to buy or sell options.

Implied volatility is not a perfect measure of future price movements.

Option prices can be affected by factors other than implied volatility.

What Is Implied Volatility?

Implied volatility is a measure of the expected volatility of a security’s price. It is derived from the stock price and the strike price of that security. The higher the implied volatility, the greater the expected price movements of the security.

Volatility is a measure of how much a security’s price changes over time. Standard deviation is one way to measure volatility. Implied volatility is different from historical volatility because it is derived from option prices, which are influenced by factors such as the level of interest rates, the amount of time until expiration, and the underlying security’s price.

Historical volatility is based on the past moves of the underlying security

How Is Implied Volatility Calculated?

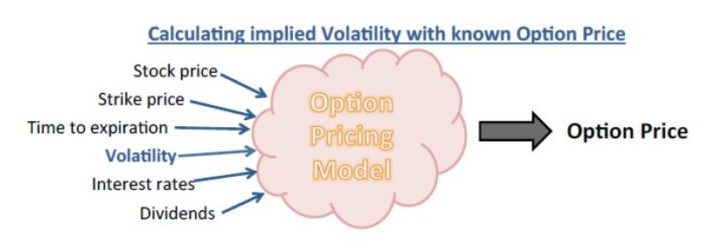

Implied volatility is calculated using an option pricing model. The most popular option pricing model is the Black-Scholes model. The Black-Scholes model is a mathematical formula that takes into account several factors, including the price of the underlying security, the strike price of the option, the time to expiration, interest rates, and dividends.

You can use an online calculator to input these factors and calculate IV. However, it’s also helpful to know how to calculate IV by hand so that you can better understand the process.

Let’s walk through an example.

Let’s walk through an example.

Suppose you’re interested in buying a call option on XYZ stock with a strike price of $50 that expires in one month. The current stock price of XYZ is $49, the risk-free interest rate is 2%, and there are no dividends.

Plugging these numbers into the Black-Scholes formula, we get an IV of 22.76%.

What does this number mean?

It means that over the next month, there is a consensus that XYZ stock will have a one standard deviation move of 49 x 22.76% = $11.15.

In other words, there’s about a 68% chance that XYZ stock will trade between $37.85 and $60.15 over the next month ($49 +/- 1 standard deviation).

Why Is IV Important?

For the options trader, implied volatility connects standard deviation (a statistical measure of volatility), the potential price range of the underlying security, and theoretical pricing models (such as Black-Scholes). By understanding how these concepts are related, you can make better-informed trading decisions—for example, whether to buy or sell options, what strike prices to target, and how long to hold your positions for.

Standard deviation is a statistical measure that quantifies the amount of variability or dispersion in a set of data points. In finance, the standard deviation is used to measure the volatility of a security’s potential price range over time.

The higher the standard deviation, the more volatile the security’s price is—meaning that it has a higher potential to move up or down over time. On the flip side, the lower the standard deviation, the less volatile the security’s price is—meaning that it has a lower potential to move up or down over time.

Implied volatility is a forward-looking measure of a security’s expected price range over a specified period. In other words, it estimates how much the security’s price could potentially move— up or down — over time.

The relationship between standard deviation and implied volatility is simple: The higher the implied volatility, the higher the expected price range (and vice versa). This relationship is important for options traders to understand because it can help them gauge how volatile a security’s price might be in the future and make better-trading decisions accordingly.

Benefits Of Using Implied Volatility

There are several benefits of using implied volatility when trading options.

Determining Whether an Option is Overpriced or Underpriced

One benefit of using implied volatility is that it can help you determine whether an option is overpriced or underpriced. If the implied volatility is higher than the historical volatility, then the option is considered to be overpriced. Conversely, if the implied volatility is lower than the historical volatility, then the option is considered to be underpriced.

Predicting Future Volatility

Another benefit of using implied volatility is that it can help you predict how volatile the underlying security will be in the future. This information can be useful in deciding when to buy or sell options. If you expect the underlying security to become more volatile, then you may want to buy options. And if you expect the underlying security to become less volatile, then you may want to sell options.

Deciding When to Buy or Sell Options

Finally, implied volatility can also help you decide when to buy or sell options. If you think that the underlying security will become more volatile, then buying call options may be a good idea. And if you think that the underlying security will become less volatile, then buying put options may be a good idea.

Risks Of Using Implied Volatility

There are also some risks associated with trading options based only on implied volatility.

Risk 1: Implied Volatility Is Not a Perfect Measure of Future Price Movements

One of the risks of trading options based on implied volatility is that it is not a perfect measure of future price movements. While implied volatility does provide some insight into how the market expects a stock to move, it is not an exact science. There can be times when the market underestimates or overestimates how much a stock will move, which can lead to losses for option traders.

Risk 2: Implied Volatility Can Change Quickly and Unexpectedly

Another risk of trading options based on implied volatility is that it can change quickly and unexpectedly. This can happen for a variety of reasons, such as changes in the underlying stock’s price or unexpected news events. When implied volatility changes, it can have a big impact on option prices. This means that traders need to be prepared for the possibility of sudden changes in market conditions.

Risk 3: Option Prices Can Be Affected by Factors Other Than Implied Volatility

In addition to the risks mentioned above, another risk of trading options based on implied volatility is that option prices can be affected by factors other than implied volatility. These other factors include things like time decay and interest rates. This means that even if the market’s expectations for a stock’s price movement haven’t changed, the price of the options could still go up or down due to these other factors.

Conclusion

Implied volatility is a measure of the expected volatility of a security’s price. It is not a guaranteed number and the standard deviation price should not be considered 100% accurate. In fact IV can change throughout the life of the options contract.

It can be helpful to compare the implied volatility with historical volatility since historical, has happened. If you find these numbers are vastly different, just remember that historical does not predict the future and neither does implied

Looking for a safe and reliable investment?

A dividend stock is a company that pays out part of its profits to shareholders in the form of dividends. This can be an attractive option for investors looking for regular income and stability in their portfolio.

We’ve put together a list of 101 of the top dividend stocks on the market today. You can download it for free by clicking the link above.

Invest in dividend stocks today and secure your financial future!